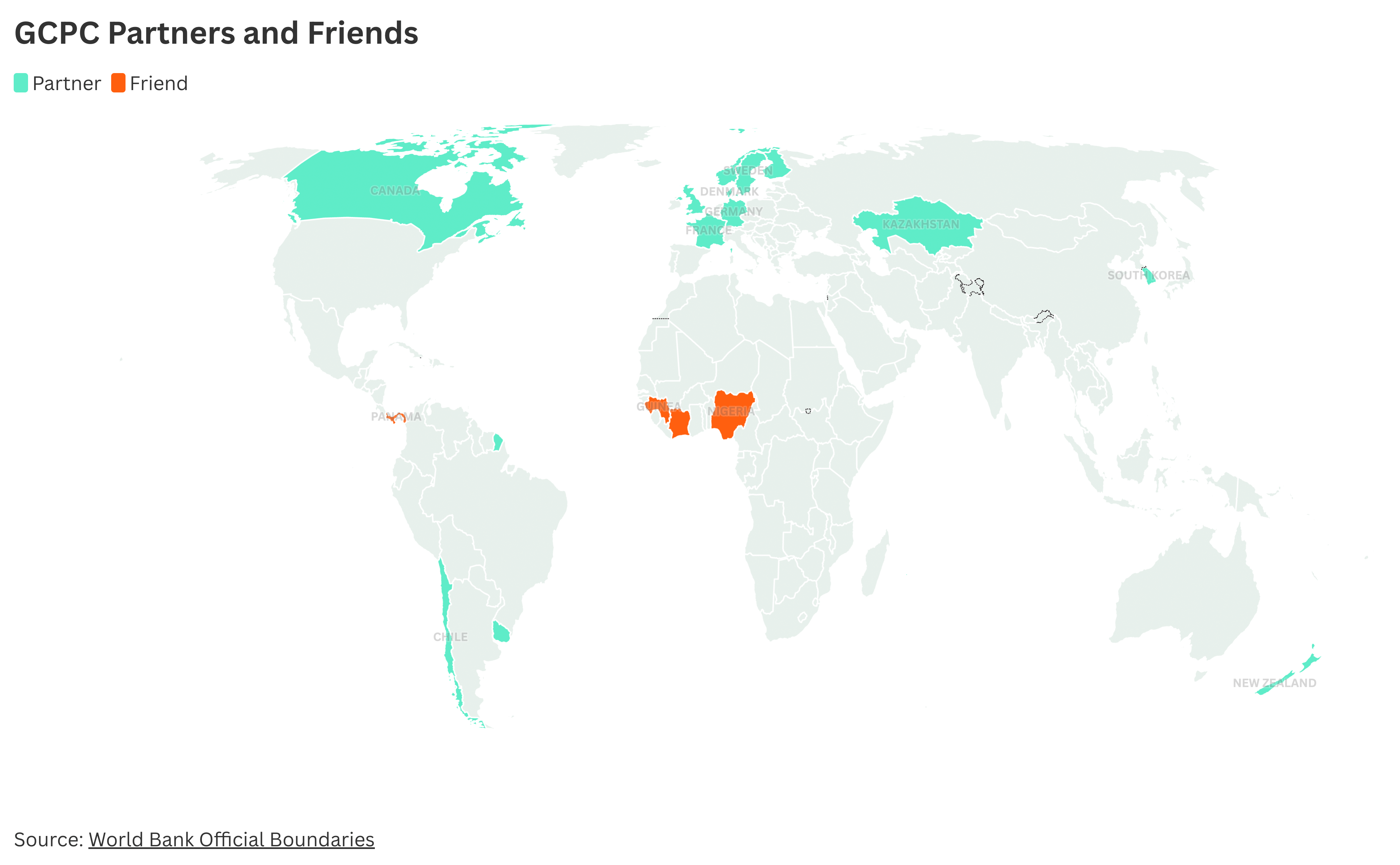

Partners of the GCPC are implementing, or scheduled to implement, carbon pricing and are committed to the goal of increasing coverage of carbon pricing to 60 percent of global emissions by 2030.

Partners & Friends of the GCPC

The GCPC thrives on collaboration and cooperation among various stakeholders. The Challenge recognizes that addressing climate change and achieving global emission reduction goals requires collective effort and knowledge-sharing.

Partners

Friends

Friends of the GCPC support the Challenge’s goals and objectives and have a clear interest in explicit carbon pricing domestically or internationally.

Partners

Canada

Since 2019, every jurisdiction in Canada has had a price on carbon pollution, covering approximately 80% of Canada’s GHG emissions. Canada’s approach is flexible: any province or territory can implement its own pricing system tailored to local needs, or can choose the federal carbon pricing system. The federal government sets minimum national stringency standards (the ‘federal benchmark’) that all systems must meet to ensure they are comparable and effective. If a province or territory decides not to price carbon pollution, or proposes a system that does not meet these standards, the federal system is put in place. Currently, the federal pricing system consists of a regulated performance-based trading system for industries, known as the Output-Based Pricing System. Proceeds from the federal pricing system remain in the province or territory of origin, with a significant portion returned directly to households to spend as they see fit. Canada’s GHG Offset Credit System encourages voluntary emissions reduction and removal activities not covered by carbon pricing, further expanding the financial incentives to reduce carbon pollution across the economy. For more information, please visit: Carbon Pollution Pricing Across Canada

Chile

Chile implemented a carbon tax in 2017 as part of the tax on air emissions from contaminating compounds. The objective of the tax is to reduce the negative impacts of fossil fuel use for the environment and public health, and it was further updated through amendments in 2020, which includes an offset system to fund emission reductions projects in Chile. The carbon tax applies to CO2 emissions from primarily the power and industry sectors. Under the new Framework Law on Climate Change (2022), an additional system of tradable emission certificates is established.

Denmark

Denmark implemented its national carbon tax in 1992, called CO2-afgift, to increase the profile of climate change and incentivize less energy consumption from carbon-intensive sources. A complementary measure to the EU Emissions Trading System (EU ETS), Denmark’s carbon tax covers much of the fuel-use not covered under the EU ETS. The tax applies to all direct greenhouse gas emissions from fossil fuels across all sectors. In 2022, Denmark adopted a Green Tax Reform with a higher and more uniform tax on both energy and non-energy emissions from the industry, non-roadgoing transport and the heating sector (with wide political support). The tax is supported by a floor price, which could be affected, if the EU’s emissions trading market acts differently than the expectations. This ensures that the price of emissions is kept high in order to keep a consistent and high incentive for companies to lower their emissions. The tax is recalculated on an annual basis to account for inflation.

European Union

The European Union launched its Emissions Trading System (EU ETS) in 2005. It is the oldest and so far largest ETS operating worldwide. The system operates in all EU Member States, plus Iceland, Liechtenstein and Norway, and Northern Ireland. Since 2020, it is also linked with Switzerland's ETS. The EU ETS applies to direct emissions from activities in the power sector, manufacturing industry, intra-EU aviation and from maritime transport from 2024. It works on a cap-and-trade principle, with the cap on emissions (expressed in emission allowances) set top-down and decreasing annually. Auctioning is the main method of distributing allowances in the EU ETS, raising revenue mostly for national budgets, but also for the ETS Innovation Fund and ETS Modernisation Fund. Between 2005 and 2022, the EU ETS has helped drive down emissions from electricity and heat generation and industrial production by over 37 percent, while generating over EUR 175 billion in auction revenue to date. The EU ETS is the central pillar of EU climate change policy in the context of the European Green Deal and European Climate Law. In 2023, the EU concluded a major reform of the EU ETS, strengthening the system’s ambition and expanding its scope to maritime sector. The reform also introduced a new ETS 2 for buildings, road transport and small-emitting industry to start in 2027. With this latest reform, all auction revenue will be directed to climate action and green energy transition.

Finland

... Text follows ...

France

France has implemented carbon pricing since 2005 through the European Union Emissions Trading System (EU ETS), which covers power generation, industry, aviation, and maritime transport. The French carbon tax (Contribution Climat-Énergie or CCE) was implemented in 2014 as part of the domestic excise taxes on energy consumption, rising over time based on carbon content of the fuels. The CCE applies to upstream CO2 emissions from all fossil fuels primarily in the industry, buildings and transport sectors (with some exceptions), which covers 35% of France’s greenhouse gas emissions. Since 2018, the domestic excise taxes no longer increased based on a carbon component.

Germany

The German national emissions trading system for heat and road transport (Nationales Emissionshandelssystem, or nEHS), came into effect in 2021, established by the Fuel Emissions Trading Act of 2019. The system covers sectors not covered under the EU Emissions Trading System (EU ETS). The nEHS is being phased in gradually with a fixed price on allowances from 2021 to 2025 and a price corridor from 2025 to 2026, with its cap based on Germany’s mitigation targets for sectors not covered by the EU ETS. The nEHS is part of a broader national package of climate measures adopted by Germany to meet its 2030 climate targets and 2050 carbon neutrality goal. The German ETS will be merged with the EU ETS2 when the latter will enter into force in 2027.

Kazakhstan

The Kazakhstan Emissions Trading System was launched in January 2013 and covers approximately half of the country’s CO2 emissions. This includes around 200 installations across the power, centralized heating, extracting industries, and manufacturing sectors. The system’s cap is determined based on expected production output and a benchmark, with an additional reserve of allowances for entities that exceed their planned output. Since 2021, all allowances have been allocated through benchmarking, and there is no limit to the offset credits that entities can use for compliance.

New Zealand

The New Zealand Emissions Trading Scheme (NZ ETS) entered into effect in 2008 and is part of a framework of policies and measures to address New Zealand’s greenhouse gas emissions. The scheme has the broadest sectoral coverage of any ETS and covers all greenhouse gasses from all sources, including the forestry, waste, transport, power, agriculture and industry sectors, however agricultural emissions have reporting obligations only. The NZ ETS was initially nested under the Kyoto Protocol with links to international Kyoto carbon markets; however, as of 2015 the system transitioned to a domestic system only. New Zealand may use high integrity international carbon markets as part of meeting its climate targets.

Norway

Norway implemented its first national carbon tax in 1991 with the goal to achieve cost-effective greenhouse gas emissions reductions. Norway has since expanded its system of taxes on greenhouse gas emissions to cover emissions from combustion of all liquid and gaseous fossil fuels, incineration of waste, CO2 and CH4 fugitive emissions, and emissions of hydrofluorocarbons, perfluorocarbons and SF6. Norway has also participated in the EU Emissions Trading System (EU ETS) since 2008. The Norwegian taxes and the EU ETS are complementary and cover different sectors in the economy. Certain activities are covered by both taxes and the EU ETS. In 2023, 84% of Norwegian emissions of all greenhouse gases and 98% of emissions of CO2 is subject to carbon pricing through either national taxes or the EU ETS.

South Korea

The Korean Emissions Trading System (K-ETS) was launched in 2015, making the Republic of Korea first in East Asia to operate a national cap-and-trade scheme. The system has since become an essential tool in meeting the country’s 2030 climate targets, with the cap established based on the Basic Roadmap for Achieving National GHG Reduction Targets. The K-ETS covers direct and indirect emissions from various sectors, including the industry, power, buildings, transport, waste, and public services.

Sweden

Sweden covered by the European Union Emissions Trading System (EU ETS). Its carbon tax (koldioxidskatt) was implemented in 1991. It aims to reduce dependency on fossil fuels and is combined with the country’s energy tax (energiskatt). The Swedish carbon tax is calculated on the basis of average fossil carbon content of all fossil fuels except peat, with an exemption for installations covered by the EU ETS.

United Kingdom

The United Kingdom has a national emissions trading scheme and a complementary carbon tax. The UK Emissions Trading Scheme (ETS) began operation in 2021, replacing the UK’s participation in the European Union’s ETS. The UK ETS plays an important role in meeting the country’s net-zero goals and from 2024 the UK ETS cap will be reset to be aligned with the UK’s net zero targets. The UK ETS covers greenhouse gas emissions in energy-intensive industries, the power sector, and aviation domestic to the UK and between the UK and the European Economic Area, Switzerland and Gibraltar. The majority of allowances distributed each year are sold at fortnightly auctions, with some allowances also given away as part of free allocations to sectors at risk of carbon leakage. The UK ETS is supported by a carbon tax covering the CO2 emissions from the power sector in Great Britain. The UK Carbon Price Support (CPS) rate is a carbon tax implemented since 2013 with the goal to spur investment in low-carbon electricity generation.

Uruguay

... Text follows ...

Friends

Côte d’Ivoire

Côte d’Ivoire joined the GCPC as a Friend in 2023. The country is committed to addressing climate change through its Nationally Determined Contribution (NDC), which aims to reduce greenhouse gas (GHG) emissions by 28% by 2030 compared to a business-as-usual scenario. Côte d’Ivoire’s climate strategy focuses on enhancing renewable energy, improving energy efficiency, and promoting sustainable agricultural practices. The country recognizes the value of carbon pricing as a key tool to mitigate GHG emissions and is exploring mechanisms to integrate carbon pricing into its national climate policy framework. By leveraging carbon pricing, Côte d’Ivoire aims to create financial incentives for reducing emissions and fostering a low-carbon economy.

Guinea

Guinea joined the GCPC as a Friend in 2024. In its revised 2021 Nationally Determined Contribution (NDC), Guinea committed to reducing its GHG emissions by 69% by 2030, with 20% unconditionally and 49% conditionally. The focus is on the energy, agriculture, and forestry sectors. Guinea's climate action plan includes increasing the share of renewable energies, improving energy efficiency, and implementing sustainable land management practices. Recognizing the importance of carbon pricing, Guinea is exploring the establishment of a carbon pricing mechanism to support its ambitious climate goals. By adopting carbon pricing, Guinea aims to encourage emission reductions and attract investments in green technologies, thus contributing to a sustainable and resilient future.

Nigeria

... Text follows …

Panama

In 2024, Panama joined the Global Carbon Pricing Coalition (GCPC) as a Friend, reinforcing its commitment to addressing climate change. The country is focused on achieving ambitious climate targets set through its NDC. Panama’s climate strategy prioritizes expanding renewable energy, improving energy efficiency, and promoting sustainable land use and forest management. By understanding the importance of carbon pricing in driving this transformation, Panama is actively exploring mechanisms such as carbon crediting mechanisms to integrate into its national climate policies, achieving cost-effective reduction of greenhouse gas emissions. By engaging with the GCPC, Panama aims to enhance its capacity, draw from global best practices, and accelerate its transition to a low-carbon economy through the effective implementation of carbon pricing initiatives.

Play your part

We welcome Partners and Friends to the GCPC.

Any country with a clear interest in carbon pricing may join as a Friend to the initiative. Friends of the GCPC may send representatives to the Technical Working Group and could participate in pilot partnerships to receive tailored support for their efforts to implement or better understand carbon pricing.

Jurisdictions with carbon pricing systems assessed by the World Bank to be “implemented” or “scheduled for implementation” are invited to join as Partners. As a partner of the GCPC, you have the opportunity to build upon your existing leadership in carbon pricing, collaborating with like-minded jurisdictions.

The GCPC also welcomes Network members from various programmes, initiatives, and subnational jurisdictions.

Collaboration

The GCPC works in harmony with existing international carbon pricing initiatives, offering a leader-level forum for dialogue to drive action and raise the profile of this effective policy tool for least-cost emissions reductions.

Spotlight on complementary initiatives

The GCPC serves to spotlight and amplify other complementary initiatives led by key international organizations such as the World Bank, the International Carbon Action Partnership (ICAP), the International Energy Agency (IEA), and the Organisation for Economic Co-operation and Development (OECD).

Concrete emissions coverage target

The GCPC sets a concrete target for emissions coverage, making it the only initiative to do so for carbon pricing. This goal contextualizes international pricing initiatives, encourages greater ambition, and allows for progress tracking over time.

International discussions

The GCPC establishes an avenue for discussing international considerations relating to carbon pricing, facilitating information exchange, and fostering collaboration among nations.